Solar Adoption Brings New Risks—And New Insurance Solutions

Solar system insurance has become essential as adoption accelerates across residential, commercial, and industrial sectors. Traditional property insurance policies are proving inadequate for today's solar systems, which go far beyond simple rooftop panels to include advanced inverters, hybrid setups, battery storage, and digital monitoring platforms. These technologies represent major investments and operational dependencies—but many remain underinsured, putting owners and developers at serious financial risk. In response, the insurance industry is developing solar-specific coverage that protects not only physical assets, but also energy output, revenue continuity, and long-term project success. For solar companies, EPCs, and large-scale users, understanding these innovations is now a vital part of risk mitigation.

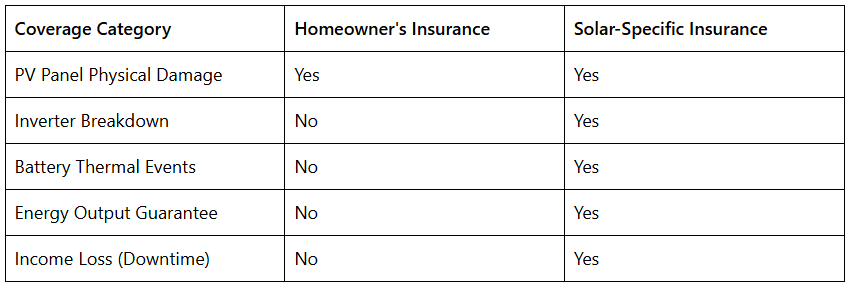

Why Standard Insurance Fails to Fully Cover Solar Systems

Traditional homeowner's or property insurance policies often treat solar systems as a static physical asset—ignoring their electrical complexity, performance dependency, and integration with energy storage. As a result, coverage may exclude:

- System underperformance or reduced energy yield

- Failures in inverters, monitoring systems, or batteries

- Lithium-ion battery thermal events or degradation

- Mounting structure damage from wind or snow loads

- Revenue loss due to weather conditions or grid instability

This gap has prompted solar system owners and financiers to demand more sophisticated insurance models—especially in commercial and utility-scale deployments where downtime translates to immediate financial loss.

The Rise of Solar-Specific Insurance Products

Insurers are increasingly offering policies tailored to the performance, durability, and operational role of solar power systems.

Performance Guarantee Insurance

This policy type ensures that a solar installation meets minimum expected output thresholds, compensating owners if production falls short. It is especially relevant for financed or third-party-owned systems, where the return on investment depends on consistent energy generation. These policies are typically backed by third-party irradiance data and performance modeling.

Battery System and Energy Storage Coverage

As hybrid and off-grid installations grow, insurers are addressing battery-specific risks—particularly for lithium iron phosphate (LiFePO₄) and lithium nickel manganese cobalt oxide (NMC) chemistries. Coverage can include:

- Fire or explosion risks

- Accelerated degradation

- Replacement costs due to thermal runaway

- Loss of storage capacity due to grid interruptions

This is critical for industrial users who rely on storage to maintain power quality or avoid peak tariffs.

Parametric Weather-Indexed Insurance

Unlike traditional policies that require physical damage claims, parametric insurance pays out automatically when predefined weather conditions—like low solar irradiance, hail, or wind speeds—are met. This model is ideal for solar farms and off-grid systems in areas prone to climate variability. Claims are processed faster, providing liquidity when it's needed most.

Revenue Protection Insurance

These policies reimburse lost revenue from solar system downtime. Whether caused by inverter failure, transmission issues, or natural disasters, the insurance cushions the financial blow of energy production loss. In regions with volatile grid conditions, this coverage helps maintain cash flow stability.

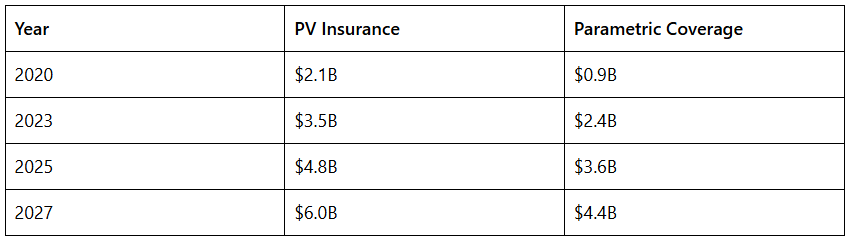

Global Market Trends and Growth of Solar Risk Coverage

The global solar insurance market is growing in tandem with the broader solar sector. With the increasing integration of storage and digital systems, total market value is projected to exceed $8 billion by 2027. Key drivers include:

- Expansion of grid-tied commercial systems in Asia

- Growth in hybrid systems in Africa and South America

- Financiers' demand for bankability and risk mitigation

- Climate change-induced volatility in weather patterns

Solar Insurance Market Forecast (USD Billion)

Source: Allied Market Research, IEA, Global Parametric Alliance

In countries like Germany, Japan, and India, solar insurance is becoming a prerequisite for project financing. In Southeast Asia and Sub-Saharan Africa, where hybrid microgrids are scaling rapidly, parametric insurance is gaining traction for its fast payouts and climate risk coverage.

Real-World Example 1: Warehouse Rooftop Solar in South Africa

A 500kW commercial rooftop solar system in Johannesburg experienced frequent inverter shutdowns due to grid instability. While the inverter manufacturer provided warranty replacements, the business faced six weeks of reduced energy output, affecting their warehouse cooling systems and operations.

The facility had secured performance insurance from Munich Re via a local solar-focused broker. Because of predefined irradiance and temperature data triggers, a payout of $24,600 was processed in just 9 days—helping the company avoid a serious operational and financial shortfall.

Real-World Example 2: Parametric Coverage in Rural India

In 2022, a mini-grid project in rural Maharashtra installed a 150kW solar-battery hybrid system. Recognizing the region's monsoon variability, the developer opted for a parametric policy tied to monthly irradiance data. When a stretch of heavy rainfall in July 2023 lowered power generation below baseline, the policy triggered an automatic payout to offset diesel generator usage costs. This helped maintain service reliability for 800 village households and small businesses.

Key Questions to Evaluate Solar Insurance Readiness

Whether you're an installer, EPC firm, investor, or business energy user, asking the right insurance questions upfront is critical:

- Does your coverage include advanced inverters and battery systems?

- Are production shortfalls compensated based on third-party data?

- Can you access regional parametric coverage for weather risks?

- Is business interruption due to solar faults covered?

- Do you have documentation (monitoring data, certifications) to support claims?

How Sunpal Energy Builds Insurance-Compatible Systems

At Sunpal Energy, our products are designed with insurability and performance reliability in mind. We help our partners reduce risk and increase financial security by delivering:

- Internationally certified components (IEC, CE, UL, TÜV)

- Real-time smart monitoring platforms

- Module efficiencies up to 23.3%

- Safe LiFePO₄ batteries with long cycle life

- 30-year linear performance warranties

- Turnkey system documentation to support insurance audits

By integrating performance transparency and component traceability, Sunpal systems align with the needs of global insurers and financiers.

Conclusion: Solar Insurance Is No Longer Optional

The rapid evolution of solar technologies—from simple rooftop arrays to complex, integrated energy ecosystems—demands an equally evolved approach to risk management. Standard insurance is not enough. Solar-specific solutions are no longer niche; they are critical infrastructure for protecting assets, revenue, and stakeholder trust.

Solar companies, developers, and end users alike must proactively evaluate insurance options, and partner with manufacturers who deliver both performance and accountability. At Sunpal, we stand behind every system with engineering precision, global compliance, and readiness for tomorrow's energy realities.

Speak with our team today to learn how Sunpal solar systems are built for bankability, protection, and long-term value.